Introduction

In today’s article we will be exploring the topic of Bridging Loans against Land with Planning: to help readers understand the benefits, processes, and best practices for using bridging loans in this context.

What is Bridging Finance?

A bridging loan can offer short-term funding solutions for investors and individuals who need an efficient solution for securing or developing property. Bridging loans can be more flexible in situations when a mortgage isn’t suitable.

Whilst a bridging loan would normally be secured against a physical building, in some circumstances, land can be used as the security.

As with a mortgage, if the borrower fails to repay the loan or adhere to the other terms, then the security may be repossessed.

Benefits of Using Bridging Finance for Land Projects

- Capitalising on Time-Sensitive Opportunities: Plots of land can often be sold at auction with completion required in 28-days. Bridging enables developers to act quickly on profitable deals and auction purchases.

- Flexibility: Bridging can be used for a variety of purposes including purchasing land, covering planning costs, or starting construction.

- No Long-Term Commitment: The short-term nature of bridging loans allows developers to repay once longer-term financing is secured. Most bridging loans run for 1 to 24 months as opposed to say 25 years for a term mortgage.This might allow a developer to apply for planning permission or refine their building costs and requirements for starting construction.

What funding is available against Land with Planning

At BIG Property Finance we can provide bridging finance against land with planning!

For us to appraise the current land value we would need to understand;

- Original Purchase price & date

- What planning is held (property footprint/size sq.ft.)

- A schedule of works & costings

- Gross Development Value

We can then look to lend up to 60% LTV of the 180-day value.

Need help financing the whole project? – Why not check out our Development Finance facilities.

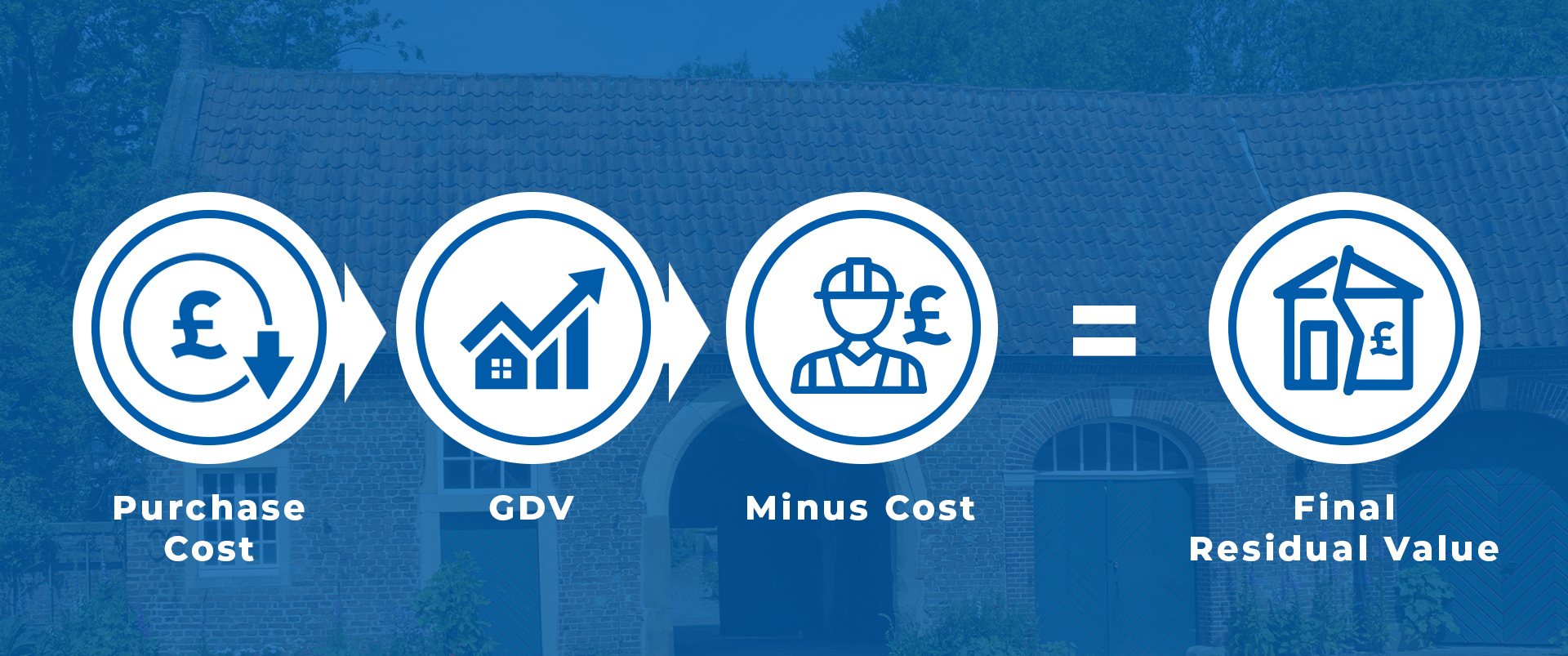

Determining Land Value

The residual land value is what’s left over once you deduct the costs/profit margin from the gross development value. The value of land can be appraised from the ultimate future use of that land and its location. Land without planning will only have significant value if it is in a very prominent/desirable location but is generally less desirable than that with planning in place or previously agreed. When appraising land without planning, at BIG, we would consider this agricultural land, which can have a value of up to £15,000 an acre. However, once planning has been agreed on land, this facilitates determining its current value by working backwards from the GDV (Gross Development Value.) If you were to take the GDV and deduct the projected constructions costs for a project, as well as other associated costs, like legal fees, finance costs and acquisition costs, you would be able to determine the ‘residual land value.’ Generally speaking, the residual land value will be around 25 to 33% of the final GDV.

Case study

Bridging loan completed against land with outline planning permission for the development of one large detached dwelling with 5 bedrooms, measuring 4010 sq.ft.

The borrower was intending to amend the planning from one large unit to two medium size properties with a view to exit onto development finance once secured.

The market in the area seemed relatively liquid, noting three properties on the market in the same post code and 21 being sold within a mile in the last year.

Our due diligence and valuation report was focused on the current planning agreed, to allow for any potential refusal or later amendments.

Gross loan provided at 60% LTV – £216,000, 6 month term.

Tips for Managing Costs and Timelines

Accurate Budgeting: Importance of detailed project costing to avoid overruns. Building projects are notorious for going over budget or resulting in unexpected costs. It’s important to take time and expertise when calculating the estimated build costs and ensuring there is some contingency.

Timeline Management: Strategies to keep the project on track, such as milestone setting and regular progress reviews. A monitoring surveyor may be used by a lender to ensure that a project is on track and whether the finances are stacking up compared to the original project projections.

Choosing the Right Lender: An important consideration for your investment is what lender you choose as interest rates and fees will be factors to consider as well as the lenders reputation.

Contingency Planning: Setting aside funds for unexpected expenses and delays

Regular Communication: Maintaining clear and consistent communication with contractors, planners, surveyors, and lenders.

Conclusion

Bridging finance may be able to facilitate the beginning of your development project by allowing you to release equity from your land.

Whilst calculating your construction costs and schedule of works is a delicate and challenging process, maybe bridging could make your goals a reality.

For more information contact BIG Property Finance on;