Bridging finance plays an integral role in the current property financing market as it encompasses the need for secured finance with the speed and flexibility that isn’t available with traditional mortgage products. Within this article we will be examining current trends in the bridging loan market and predicting future developments, this will include the consideration of emerging technologies, and market shifts.

Mintel expects the value of the bridging loans market to reach £10.9 billion by the end of 2024 with 25% growth expected over the next five years. (Cone, 2024)

Current Trends

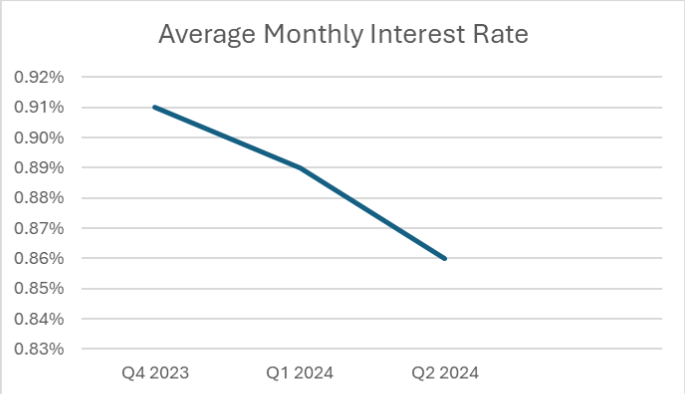

Site Bridging Trends has reported bridging loan figures for Q2 2024 as follows;

Average monthly interest rate at 0.86%, slightly down from Q1 2024 at 0.89% and again from Q4 2023 at 0.91%. Average completion time, 52 Days. Average transaction, 54.2% unregulated, average LTV 59.3%, average Term 12 Months. Demand for business funding has dropped considerably since Q1 2024, from 15% to just 9% with the proportion of second charge loans hitting a three-year high. Preventing a chain break was the most popular use of bridging finance in Q2 2024 while demand for auction funding saw the biggest uplift, rising from 9% in Q1 to 14%. (BridgingTrends, 2024).

Bridging Trends is a quarterly publication developed by short-term finance lender, MT Finance, to offer a general snapshot of the bridging finance sector.

History of Bridging

Bridging finance, a relatively recent financial product, first emerged in the 1960s. Initially, banks and building societies offered it to homeowners who needed to buy a new house before their existing property had sold. The term “bridging finance” likely comes from its purpose of “bridging the gap” between the purchase of a new home and the sale of an old one.

Bridging finance, a relatively recent financial product, first emerged in the 1960s. Initially, banks and building societies offered it to homeowners who needed to buy a new house before their existing property had sold. The term “bridging finance” likely comes from its purpose of “bridging the gap” between the purchase of a new home and the sale of an old one.

By the late 1980s, the market saw an increase in available funding due to unmet demand. Buy-to-let investors began using bridging finance to refurbish properties before renting them out, to expedite transactions, or to finance auction purchases. This shift was influenced by the introduction of Assured Shorthold Tenancies under the Housing Act of 1988, which, although not directly linked to bridging loans, played a crucial role in the industry’s evolution—though few recognised its significance at the time.

In the early 2000s, the mortgage market saw a dramatic increase as High Street lenders significantly relaxed their lending criteria. This led to a sharp rise in property prices due to growing demand. However, the relaxed criteria also resulted in many borrowers taking on mortgages they couldn’t afford. During financial hardships, bridging loans became a critical option for those in need, with many opting for bad credit bridging loans while attempting to sell their properties. (Hemming, 2024)

Key predictions

The bridging finance market is expected to undergo significant changes over the next five years. Here are some key predictions:

1. Growth in Demand

-

Increased Popularity: Bridging finance is likely to continue growing in popularity, driven by the need for quick access to funds for property purchases, particularly in competitive property markets. The flexibility and speed of bridging loans make them attractive for investors and developers.

-

Post-Pandemic Recovery: The property market’s recovery post-pandemic is expected to fuel demand for short-term financing solutions as more investors seek to capitalise on opportunities.

2. Regulatory Developments

-

Stricter Regulations: As the market grows, there may be increased regulatory scrutiny to ensure responsible lending practices. This could lead to more stringent regulations, impacting how lenders operate and the accessibility of these loans.

-

Increased Transparency: Regulations may also push for greater transparency in terms of fees, interest rates, and loan terms, benefiting consumers. For borrowers, having reliable and consistent options for bridging loan providers has only got to be a positive outcome to support their ongoing property financing needs long term.

3. Interest Rates and Economic Conditions

-

Interest Rate Fluctuations: The global economic environment and central banks’ monetary policies will influence the cost of borrowing. With the base rate finally starting to reduce after its substantial increase in the last three years, from 0.1% in 2021 to 5.25% by 2023, we saw the Bank of England finally cut interest rates to 5% at its August meeting after holding them at 5.25% seven times in a row.

In May, the International Monetary Fund (IMF) recommended that UK interest rates should fall to 3.5% by the end of 2025. The organisation, which advises its members on how to improve their economies, acknowledged that the Bank had to balance the risk of not cutting too quickly before inflation is under control.

But in its latest forecast, the IMF warned that persistent inflation in countries including the UK and US might mean interest rates have to stay “higher for even longer”. (Peachey, 2024)

If interest rates rise, the cost of bridging loans may increase, potentially dampening demand. However, the need for quick financing may keep the market active.

-

Economic Uncertainty: Economic fluctuations or uncertainties, such as inflation or recession fears, might drive more businesses and individuals to seek bridging finance as a short-term solution.

4. Technological Advancements

-

Digitalisation: The adoption of technology in the bridging finance sector will likely increase. This could include the use of AI and machine learning for credit assessments, blockchain for faster transactions, and digital platforms to streamline the loan application process.

-

Fintech Collaboration: Partnerships between traditional lenders and fintech companies could lead to innovative products and services, making bridging finance more accessible and efficient.

5. Market Competition and New Entrants

-

Increased Competition: The market is expected to see more competition as new lenders enter the space, attracted by the profitability of short-term lending. This could lead to more competitive interest rates and better terms for borrowers. The potential impact for lenders is that the smaller or less established firms may get pushed out of business if they are unable to compete on price or efficiency.

-

Specialised Products: Lenders may develop more specialised bridging finance products tailored to specific market segments, such as property developers, small businesses, or individuals with complex financial needs.

6. Impact of Green and Sustainable Finance

-

Sustainability Focus: The trend towards sustainable and green finance could influence the bridging finance market. Lenders might offer products that support eco-friendly property developments or energy-efficient refurbishments, aligning with broader environmental goals.

7. Globalisation and Cross-Border Lending

Cross-Border Opportunities: As property investment becomes more globalised, there may be an increase in cross-border bridging loans. This could open up new markets and opportunities for both lenders and borrowers, especially in emerging markets.

Conclusion

In summary, while the bridging finance market is expected to grow, it will also face challenges such as regulatory changes, economic fluctuations, and increasing competition. However, technological advancements and a focus on sustainable finance are likely to create new opportunities in the sector.

The overall outlook looks positive for borrowers if interest rates can remain at current levels or reduce over time, with the potential of increased competition in the market increasing opportunities and availability.

Stay informed and consider how these trends might impact your financial decisions.

For more information on your bridging finance options, contact BIG Property Finance on; info@bigpropertyfinance.co.uk – 0121 348 7830.

References

BridgingTrends. The latest Bridging Trends. 1 April 2024. 12 08 2024.

Cone, Lewis. UK Bridging Loans Market Report 2024. 12th August 2024.

Hemming, Gary. The History Of Bridging Loans. April 2024. Article. 19th August 2024.

Peachey, Kevin. Mortgage rates: How do UK interest rates affect me? 14th August 2024. News Article. 19th August 2024.